Home Depot (HD) and Lowe's (LOW) are good stocks for those who want to invest in home-improvement companies. So, investors should keep a close watch on the recovery of the housing market if they wish to benefit from these two companies.

According to Home Improvement Research Institute, the housing market surged to six-year highs last November, growing 22.7% year over year. In addition, sales of existing homes also increased over 10% as compared to last year. This was almost in line with HIRI's projection of 20% growth in housing and 9.8% increase in existing home sales for 2013. Looking forward, these numbers are expected to be around 30% and 9.3%, respectively, for 2014.

Let us see in detail what the prospects are for these firms and how will they will benefit investors.

Taking a Close Look

Home Depot is the largest American retailer for home improvement and construction products and services. Its recent results were better than consensus estimates. This was mainly driven by a rebound in the seasonal categories due to the recovering housing market in the U.S. Revenue increased on account of strong growth in comps, with an increase in earnings over last year.

A similar trend was seen for Lowe's, which reported significant growth. Backed by a solid performance across all its products, Lowe's earnings beat the estimates. Its gross profit increased 11.6% year over year. This resulted in an increase in earnings that were ahead of analysts' expectations.

In accordance with the projections from HIRI, Fitch has also predicted higher spending on home improvement in 2014. According to the National Association of Home Builders, housing market activity in 52 of approximately 350 metro areas in the U.S. has returned to or exceeded pre-recessionary levels.

All these facts indicate that the housing market is expected to grow in the future and this is a big opportunity for companies like Home Depot, Lowe's and Lumber Liquidators. Home Depot is the largest of the three in terms of store count, and it is concentrating less on expanding store count but improving store efficiency with the help of technology.

Road Ahead

To increase its presence in California market, Lowe's has acquired Orchard Supply Hardware, which is offering stiff competition to Home Depot. This will add 72 more stores to its existing fleet.

Looking forward, both companies would benefit from the booming housing industry. Home Depot, being the largest, has an edge and is better positioned to maximize its gains from the opportunity. Home Depot is working hard to attract as many customers during the holiday season. Keeping this in mind, it recently launched a mobile app for customers which will make shopping easier. Also, it is enhancing its website to make its online operations even better.

In addition, it is launching new products such as the Nest Protect smoke detector, a carbon monoxide detector, the Cree True White bulb, and many other products. It is also improvising its products to attract more customers.

Talking about Lumber Liquidators (LL), it caters to the hardwood flooring market. Currently at a P/E ratio of 30, it is very expensive as compared to both Lowe's and Home Depot. Home Depot has a P/E ratio of 20 while Lowe's is slightly more expensive at 22 times earnings. It will be better on the part of investors to look for either Home Depot or Lowe's, as they are comparably cheaper.

Making a Choice

Among all three, Home Depot looks the best in class. It is the cheapest and has a strong market position along with a wide store network. Looking at all these factors Home Depot looks to be a better investment option.

Home Depot (HD) and Lowe's (LOW) are good stocks for those who want to invest in home-improvement companies. So, investors should keep a close watch on the recovery of housing market if they wish to benefit from these two companies.

According to Home Improvement Research Institute, the housing market surged to six year highs last November, growing 22.7% year over year. In addition, sales of existing homes also increased over 10% as compared to last year. This was almost in line with HIRI's projection of 20% growth in housing and 9.8% increase in existing home sales for 2013. Looking forward, these numbers are expected to be around 30% and 9.3%, respectively, for 2014.

Let us see in detail what the prospects are for these firms and how will they will benefit investors.

Taking a Close Look

Home Depot is the largest American retailer for home improvement and construction products and services. Its recent results were better than consensus estimates. This was mainly driven by a rebound in the seasonal categories due to the recovering housing market in the U.S. Revenue increased on account of strong growth in comps, with an increase in earnings over last year

A similar trend was seen for both Lowe's, which reported significant growth. Backed by a solid performance across all its products, Lowe's earnings beat the estimates. Its gross profit increased 11.6% year over year. This resulted in an increase in earnings that were ahead of analysts' expectations.

In accordance with the projections from HIRI, Fitch has also predicted higher spending on home improvement in 2014. According to the National Association of Home Builders, housing market activity in 52 of approximately 350 metro areas in the U.S. has returned to or exceeded pre-recessionary levels.

All these facts indicate that the housing market is expected to grow in the future and this is a big opportunity for companies like Home Depot, Lowe's and Lumber Liquidators. Home Depot, is the largest of the three in terms of store count, and it is concentrating less on expanding store count but improving store efficiency with the help of technology.

Road Ahead

To increase its presence in California market, Lowe's has acquired Orchard Supply Hardware, which is offering stiff competition to Home Depot. This will add 72 more stores to its existing fleet.

Looking forward, both companies would benefit from the booming housing industry. Home Depot, being the largest, has an edge and is better positioned to maximize its gains from the opportunity. Home Depot is working hard to attract as many customers during the holiday season. Keeping this in mind, it recently launched a mobile app for customers which will make shopping easier. Also, it is enhancing its website to make its online operations even better.

In addition, it is launching new products such as the Nest Protect smoke detector, a carbon monoxide detector, the Cree True White bulb, and many other products. It is also improvising its products to attract more customers.

Talking about Lumber Liquidators, it caters to the hardwood flooring market. Currently at a P/E ratio of 30, it is very expensive as compared to both Lowe's and Home Depot. Home Depot has a P/E ratio of 20 while Lowe's is slightly more expensive at 22 times earnings. It will be better on the part of investors to look for either Home Depot or Lowe's, as they are comparably cheaper.

Making a Choice

Among all three, Home Depot looks the best in class. It is the cheapest and has a strong market position along with a wide store network. Looking at all these factors Home Depot looks to be a better investment option.

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

HD STOCK PRICE CHART

76.58 (1y: +5%) $(function(){var seriesOptions=[],yAxisOptions=[],name='HD',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1366174800000,72.8],[1366261200000,72.48],[1366347600000,74],[1366606800000,73.86],[1366693200000,73.38],[1366779600000,73.28],[1366866000000,73.37],[1366952400000,73.35],[1367211600000,73.67],[1367298000000,73.35],[1367384400000,72.76],[1367470800000,73.33],[1367557200000,73.96],[1367816400000,75.26],[1367902800000,75.07],[1367989200000,75.42],[1368075600000,75.87],[1368162000000,76.01],[1368421200000,76.67],[1368507600000,77.32],[1368594000000,77.88],[1368680400000,76.75],[1368766800000,76.86],[1369026000000,76.76],[1369112400000,78.71],[1369198800000,79.69],[1369285200000,78.91],[1369371600000,78.99],[1369717200000,79.82],[1369803600000,79.49],[1369890000000,79.44],[1369976400000,78.66],[1370235600000,79.08],[1370322000000,76.63],[1370408400000,75.1],[1370494800000,77.26],[1370581200000,78.74],[1370840400000,77.73],[1370926800000,77.61],[1371013200000,76.4],[1371099600000,76.53],[1371186000000,76.59],[1371445200000,76.14],[1371531600000,77.19],[1371618000000,75.93],[1371704400000,73.87],[1371790800000,73.82],[1372050000000,73.51],[1372136400000,74.14],[1372222800000,75.67],[1372309200000,76.27],[1372395600000,77.47],[1372654800000,76.87],[1372741200000,77.31],[1372827600000,77.73],[1373000400000,78.29],[1373259600000,79.22],[1373346000000,79.7],[1373432400000,79.4],[1373518800000,79.86],[1373605200000,80.54],[1373864400000,80.4],[1373950800000,80.22],[1374037200000,80.44],[1374123600000,80.02],[1374210000000,79.89],[1374469200000,80],[1374555600000,80.19],[1374642000000,80.27],[1374728400000,78.99],[1374814800000,78.74],[1375074000000,78.67],[1375160400000,78.6],[1375246800000,79.03],[1375333200000,78.64],[1375419600000,80.23],[1375678800000,79.66],[1375765200000,80.05],[1375851600000,78.83],[1375938000000,80.04],[1376024400000,78.97],[1376283600000,79.2],[1376370000000,79.44],[1376456400000,77.44],[1376542800000,75.14],[1376629200000,75.38],[1376888400000,75.21],[13769748! 00000,74..29],[1377061200000,73.73],[1377147600000,74],[1377234000000,73.89],[1377493200000,75.43],[1377579600000,74.12],[1377666000000,75.03],[1377752400000,75.05],[1377838800000,74.49],[1378184400000,73.9],[1378270800000,74.14],[1378357200000,72.99],[1378443600000,72.7],[1378702800000,73.58],[1378789200000,74.6],[1378875600000,75.04],[1378962000000,75.4],[1379048400000,75.11],[1379307600000,75.54],[1379394000000,75.8],[1379480400000,77.37],[1379566800000,78.51],[1379653200000,77],[1379912400000,75.91],[1379998800000,76.04],[1380085200000,75.52],[1380171600000,76.07],[1380258000000,75.96],[1380517200000,75.85],[1380603600000,76.26],[1380690000000,76.32],[1380776400000,75.88],[1380862800000,75.78],[1381122000000,75.13],[1381208400000,74.27],[1381294800000,74.14],[1381381200000,75.51],[1381467600000,76.32],[1381726800000,76.35],[1381813200000,75.18],[1381899600000,74.94],[1381986000000,75.74],[1382072400000,74.69],[1382331600000,74.62],[1382418000000,74.86],[1382504400000,75.08],[1382590800000,76.78],[1382677200000,76.25],[1382936400000,76.06],[1383022800000,77.5],[1383109200000,77.88],[1383195600000,77.89],[1383282000000,76.99],[1383544800000,77],[1383631200000,76.65],[1383717600000,76.42],[1383804000000,75.69],[1383890400000,75.48],[1384149600000,75.37],[1384236000000,76.18],[1384322400000,77.6],[1384408800000,78.94],[1384495200000,80.03],[1384754400000,79.67],[1384840800000,80.38],[1384927200000,79.75],[1385013600000,79.83],[1385100000000,79.18],[1385359200000,79.75],[1385445600000,80.35],[1385532000000,80.66],[1385704800000,80.67],[1385964000000,79.77],[1386050400000,78.71],[1386136800000,78.4],[1386223200000,78.54],[1386309600000,79.84],[1386568800000,79.6],[1386655200000,78.61],[1386741600000,79],[1386828000000,78.53],[1386914400000,79.01],[1387173600000,79.1],[1387260000000,78.62],[1387346400000,80.05],[1387432800000,79.95],[1387519200000,80.04],[1387778400000,80.56],[1387864800000,80.64],[1388037600000,81.55],[1388124000000,81.64],[1388383200000,81.94],[1388469600000,82.34],[1388642400000,82.02],! [138872880! 0000,81.89],[1388988000000,81.1],[1389074400000,81.5],[1389160800000,81.93],[1389247200000,81.57],[1389333600000,82.01],[1389592800000,80.97],[1389679200000,81.01],[1389765600000,81.07],[1389852000000,81.26],[1389938400000,81],[1390284000000,80.46],[1390370400000,80.2],[1390456800000,80.24],[1390543200000,79.16],[1390802400000,78.94],[1390888800000,78.54],[1390975200000,76.68],[1391061600000,76.93],[1391148000000,76.85],[1391407200000,75.09],[1391493600000,74.97],[1391580000000,75.26],[1391666400000,76.16],[1391752800000,76.45],[1392012000000,76.41],[1392098400000,76.7],[1392184800000,77.28],[1392271200000,77.59],[1392357600000,77.93],[1392703200000,77.57],[1392789600000,76.45],[1392876000000,77.48],[1392962400000,77.74],[1393221600000,77.87],[1393308000000,80.98],[1393394400000,81.7],[1393826400000,82],[1393912800000,82.87],[1393999200000,82.91],[1394085600000,82.41],[1394172000000,82.55],[1394427600000,82.18],[1394514000000,81.29],[1394600400000,80.56],[1394686800000,78.8],[1394773200000,79.38],[1395032400000,79.58],[1395118800000,79.82],[1395205200000,79.75],[1395291600000,80.09],[1395378000000,80.42],[1395637200000,79.66],[1395723600000,79.47],[1395810000000,78.87],[1395896400000,78.68],[1395982800000,78.72],[1396328400000,79.38],[1396414800000,79.95],[1396501200000,79.4],[1396587600000,78.72],[1396846800000,77.13],[1396933200000,77.11],[1397019600000,77.76],[1397106000000,76.78],[1397192400000,75.7],[1397451600000,75.97],[1397538000000,75.89],[1397624400000,76.58],[1397708759000,76.58],[1397708759000,76.58],[1397660406000,76.58]]};var reporting=$('#reporting');Highcharts.setOptions({lang:{rangeSelectorZoom:""}});var chart=new Highcharts.StockChart({chart:{renderTo:'container_chart',marginRight:20,borderRadius:0,events:{load:function(){var chart=this,axis=chart.xAxis[0],buttons=chart.rangeSelector.buttons;function reset_all_buttons(){$.each(chart.rangeSelector.buttons,function(index,value){value.setState(0);});series=chart.get('HD');series.remove();} buttons[0].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[0].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php?symbol=HD&ser=1d',function(data){if(data!=null){var extremes=axis.getExtremes();axis.setExtremes(data[1][0][0],data[1][data[1].length-1][0]);chart.addSeries({name:'HD',id:'HD',color:'#4572A7',data:data[1]});if(data[0][1]>=0){display=data[0][0]+" (1D: +"+data[0][1]+"%)";reporting.html(display);}else{display=data[0][0]+" (1D: "+data[0][1]+"%)";r

Reed Saxon/APToyota's North American headquarters in Torrance, Calif. As part of a companywide overhaul, Toyota Motor (TM) is planning to move its sales and marketing headquarters to suburban Dallas from Torrance, Calif., according to reports. The company will restructure its marketing arm, which currently is based in Torrance in southern California, and houses about 5,300 employees, who are being offered a redundancy package under the reorganization that is set to begin Thursday. The move would put Toyota's management closer to its operations that produce cars for the U.S. market and would reduce production costs. It is still unclear how many employees will be asked to move from the Torrance unit and how much time would elapse before the transition is complete. Employees "whose positions are significantly different in the new organization have been provided with several options, including applying for opportunities within the new marketing organization or in other departments at [Toyota Motor Sales] or Toyota Financial Services," the company said, according to the Wall Street Journal. The Japanese automaker has vehicle assembly plants in Kentucky, Indiana, Texas and Mississippi, along with technical centers in Michigan and California, while its manufacturing operations headquarters for the U.S. market is based in Erlanger, Ky. About 71 percent of the vehicles Toyota sells in the U.S. are manufactured at its 14 manufacturing facilities, up from 55 percent in 2008 and, last year, Toyota sold 2.24 million cars and light trucks, down from a record 2.62 million sold in 2007, reports said. Related According to Los Angeles Times, Torrance's Mayor Frank Scotto didn't know of Toyota's plans to move base but added that he knew that the company was supposed to make a corporate announcement Monday. "When any major corporation is courted by another state, it's very difficult to combat that," Scotto said, according to the Times. "We don't have the tools we need to keep major corporations here," he said. States such as New York and Texas have been promising financial incentives to convince California-based companies to move, using the west coast state's higher cost of operations, such as higher labor compensation and liability insurance, as an incentive, according to Scotto. Toyota Motor Sales U.S.A. and Toyota Financial Services, both of which are based in Torrance, together employ more than 9,400 people in the U.S. Toyota isn't the first to desert California in search of lower operating costs. In 2006, Nissan Motor shifted its headquarters to Nashville, Tenn., from Gardena, Calif. while Honda Motor (HMC) moved a small number of top-level employees to Columbus, Ohio, from Torrance in 2013, reports said.

Reed Saxon/APToyota's North American headquarters in Torrance, Calif. As part of a companywide overhaul, Toyota Motor (TM) is planning to move its sales and marketing headquarters to suburban Dallas from Torrance, Calif., according to reports. The company will restructure its marketing arm, which currently is based in Torrance in southern California, and houses about 5,300 employees, who are being offered a redundancy package under the reorganization that is set to begin Thursday. The move would put Toyota's management closer to its operations that produce cars for the U.S. market and would reduce production costs. It is still unclear how many employees will be asked to move from the Torrance unit and how much time would elapse before the transition is complete. Employees "whose positions are significantly different in the new organization have been provided with several options, including applying for opportunities within the new marketing organization or in other departments at [Toyota Motor Sales] or Toyota Financial Services," the company said, according to the Wall Street Journal. The Japanese automaker has vehicle assembly plants in Kentucky, Indiana, Texas and Mississippi, along with technical centers in Michigan and California, while its manufacturing operations headquarters for the U.S. market is based in Erlanger, Ky. About 71 percent of the vehicles Toyota sells in the U.S. are manufactured at its 14 manufacturing facilities, up from 55 percent in 2008 and, last year, Toyota sold 2.24 million cars and light trucks, down from a record 2.62 million sold in 2007, reports said. Related According to Los Angeles Times, Torrance's Mayor Frank Scotto didn't know of Toyota's plans to move base but added that he knew that the company was supposed to make a corporate announcement Monday. "When any major corporation is courted by another state, it's very difficult to combat that," Scotto said, according to the Times. "We don't have the tools we need to keep major corporations here," he said. States such as New York and Texas have been promising financial incentives to convince California-based companies to move, using the west coast state's higher cost of operations, such as higher labor compensation and liability insurance, as an incentive, according to Scotto. Toyota Motor Sales U.S.A. and Toyota Financial Services, both of which are based in Torrance, together employ more than 9,400 people in the U.S. Toyota isn't the first to desert California in search of lower operating costs. In 2006, Nissan Motor shifted its headquarters to Nashville, Tenn., from Gardena, Calif. while Honda Motor (HMC) moved a small number of top-level employees to Columbus, Ohio, from Torrance in 2013, reports said.

Enlarge Image

Enlarge Image  Earnings Wall

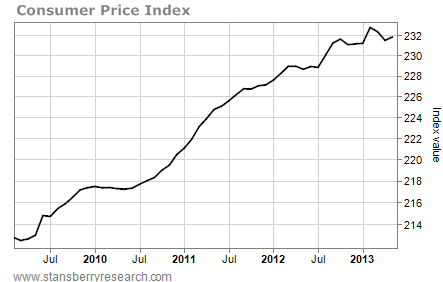

Earnings Wall  We don't really feel the pain as prices increase slowly. We're like the proverbial frog in the simmering pot of water. But it looks like things are about to heat up...

We don't really feel the pain as prices increase slowly. We're like the proverbial frog in the simmering pot of water. But it looks like things are about to heat up...  The 30-year rate has broken out above the first resistance line and is now headed toward the next resistance line near 4.4%. It's 30% higher than where it was in May. And it's up 50% from its bottom last August. Rates don't rise like this if the market is comfortable with inflation.

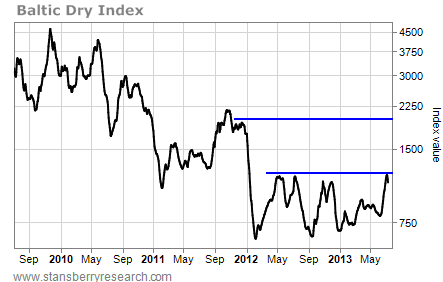

The 30-year rate has broken out above the first resistance line and is now headed toward the next resistance line near 4.4%. It's 30% higher than where it was in May. And it's up 50% from its bottom last August. Rates don't rise like this if the market is comfortable with inflation.  The BDI reflects the cost of shipping dry goods overseas. It's a good measure of economic activity. But it's an even better measure of pent-up inflationary pressures. The cost of shipping dry goods gets worked into the final cost of those commodities. After a three-year downtrend, the chart is poised to reverse to the upside. The BDI has already rallied more than 50% so far in 2013. If it can break above resistance at about 1,200, it will be poised to make a run at the next resistance level near 2,000. That will be one heck of a move for the BDI. And it will be a sure sign that inflation is heating up. – Jeff Clark

The BDI reflects the cost of shipping dry goods overseas. It's a good measure of economic activity. But it's an even better measure of pent-up inflationary pressures. The cost of shipping dry goods gets worked into the final cost of those commodities. After a three-year downtrend, the chart is poised to reverse to the upside. The BDI has already rallied more than 50% so far in 2013. If it can break above resistance at about 1,200, it will be poised to make a run at the next resistance level near 2,000. That will be one heck of a move for the BDI. And it will be a sure sign that inflation is heating up. – Jeff Clark